US Multifamily: Market Fundamentals Challenged, but Long-term Tailwinds Still Intact

سجل بريدك الالكتروني للحصول على احدث المقالات والتقارير

Key Highlights

- Ten consecutive interest rate hikes by the US Federal Reserve (“the Fed”), as well as recessionary fears, has impacted multifamily real estate fundamentals during the second half of 2022. This has lead to a deceleration in annual rent growth, rise in cap rates, and an increase in vacancy rates. This results in lower prospective asset prices.

- Investment sales volume for apartments in 2022 was the second highest on record despite significant drop year-over-year (YoY). Ample dry powder for North American commercial real estate suggests sales activity may experience some level of cushion in the event of a negative downturn.

- The increase in financing and construction costs have hurt home affordability. While this is unfavorable for developers, it could benefit current multifamily CRE owners, as rising replacement costs make their properties more valuable in the long term.

- Despite short-term headwinds facing multifamily properties, investors’ long-term perspective for multifamily properties remains strong. Opportunities in this sector stems from the large millenial and gen Z population (potential new homeowners), who currently prefer to rent rather than assume financing for property acquisition.

Multifamily Sector Grappled with Softening Fundamentals

The US multifamily housing market achieved record-setting performance in 2021 which continued well into 2022. However, the interest rate hikes that have been implemented by the Fed to combat the rapidly rising inflation has affected the multifamily property market; this stems from the increasing costs of financing, construction and insurance associated with CRE. The interest rate hikes have resulted in an exponential rise in the cost of mortgages and hedging instruments, which has created downward pressure on demand for real estate.

Historically, the multifamily sector has proved to be resilient during recessions. The current multifamily vacancy rates are well below previous recessionary levels, and rental growth remains strong. Even during the Global Financial Crisis (GFC), apartments (used as a proxy for multifamily properties) encountered a minimal vacancy rate increase of just 0.75% versus a rise of about 2.75% in other property sub-asset classes as per Cushman & Wakefield. Similarly, cumulative rental losses were also moderate at 3.75% for apartments, compared to as much as 13% for other real estate sub-asset classes.

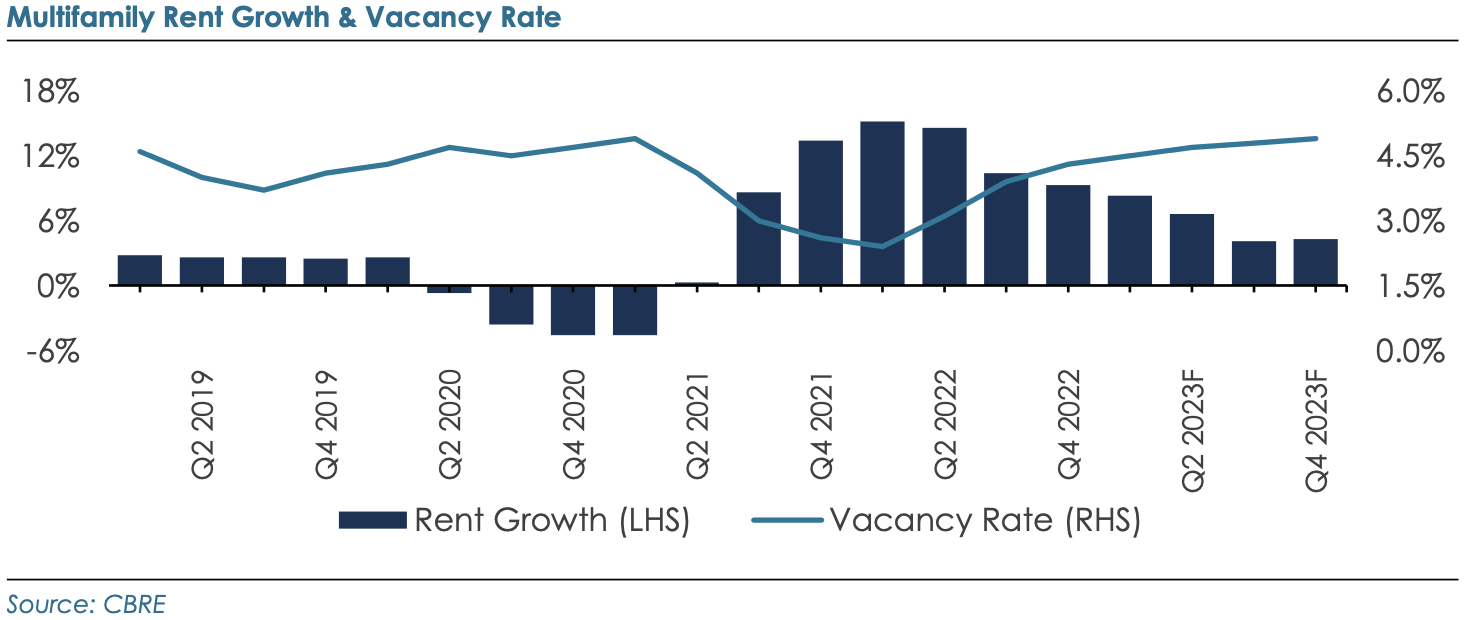

The combination of slower demand due to economic uncertainty and relatively higher new supply have led to the rise in vacancy rates. According to CBRE, the multifamily vacancy rate rose from 2.4% in Q1 2022 to 4.3% in Q4 2022. Vacancy rates have been rising since Q1 2022 and are expected to reach about 5% by the end of 2023. The year-over-year rent growth has slowed from 15.2% in Q1 2022 to 9.3% in Q4 2022. CBRE expects rental growth to slow from the double-digit growth rate during the past two years to 4.3% by Q4 2023. As effective rental growth cooled in the second half of 2022, landlords offering concessions increased across all classes. According to Fannie Mae, nearly 13% of class A properties and 9.5% of class C properties were offering concessions as of the fourth quarter of 2022, rising from mid-year levels of 10.4% and 5.3%, respectively.

Elevated Apartment Prices Set to Moderate

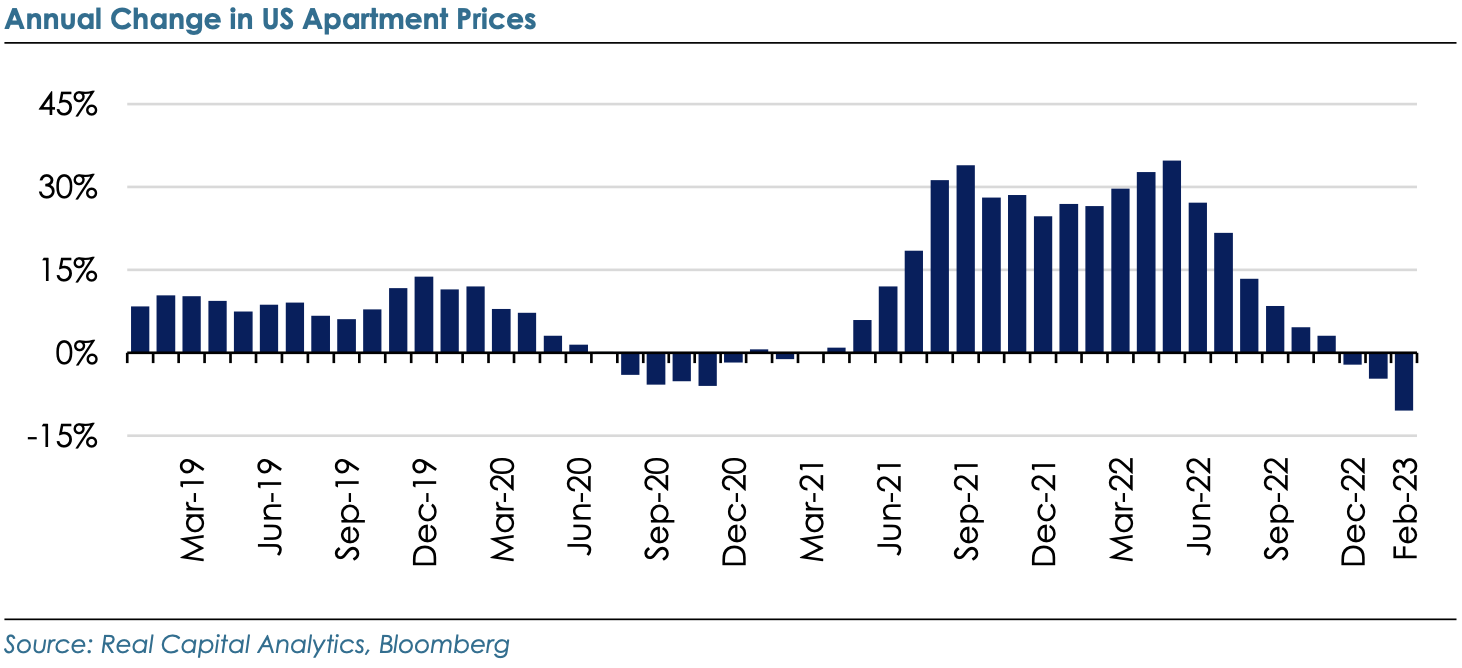

Despite the ongoing correction in apartment prices over past few months, multifamily has witnessed an asset value appreciation for the twelve months period between June 2021 and June 2022. To put into context – apartment prices rose by nearly 37% in the three years from September 2019 to September 2022. According to Real Capital Analytics, apartment prices experienced year-over-year growth rate of above 20% in each month through the first half of 2022.

However, due to the market upheaval, price growth slowed in the second half of 2022. Notably, apartment prices declined for the first time in December 2022, a reversal from the consistent year-over-year rise in each month since April 2021. The prices fell a further 4.7% and 10.5% in the first two months of 2023.

Ample Dry Powder Affords Healthy Investor Appetite

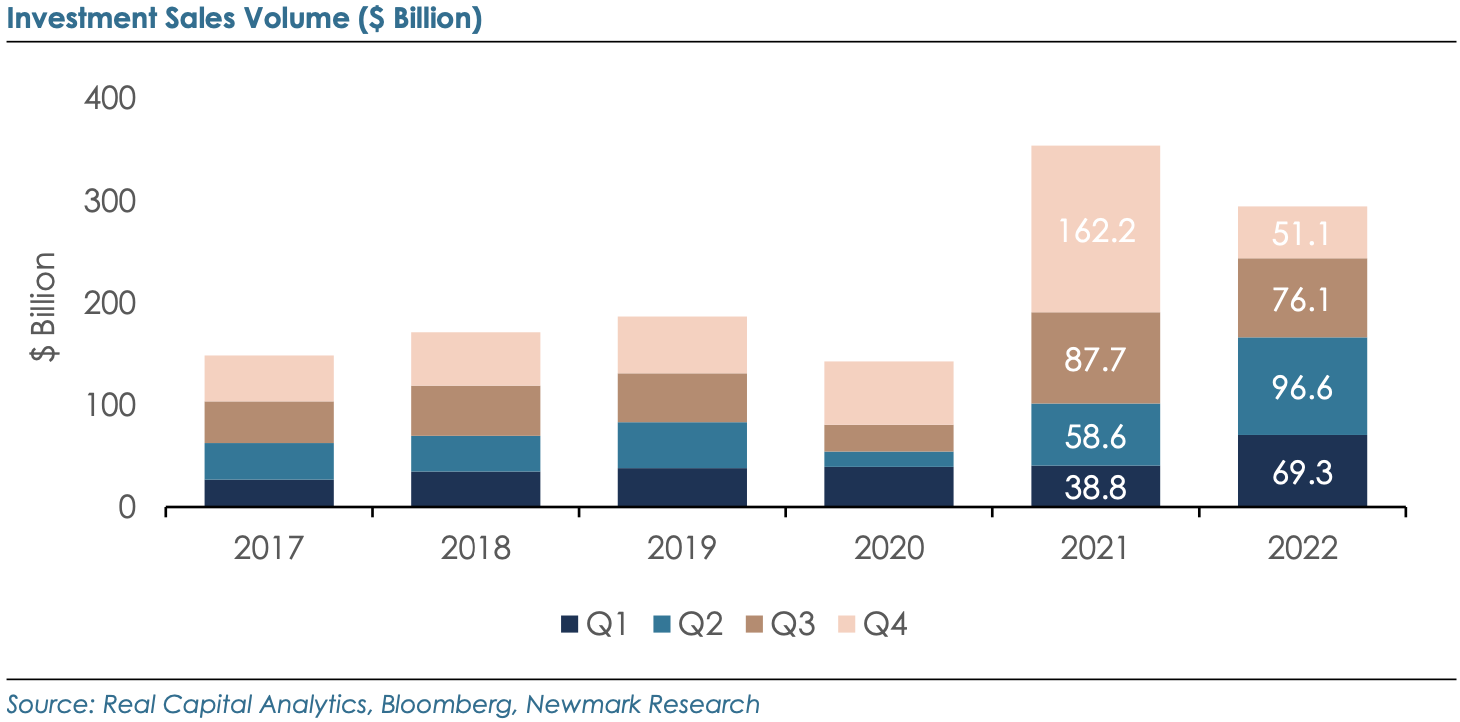

While investment sales volume declined 15.6% YoY to $293 billion in 2022, it remained the second largest annual total on record and stood 75% greater than the pre-pandemic annual average of $168.1 billion from 2015-2019. Notably, the annual decline in Q4 2022 sales volume was quite steep – total transaction volume tumbled nearly 69% year-over-year to $51.1 billion.

According to research by Newmark there is c. $234 billion in dry powder (uninvested capital) allocated for North American commercial real estate, which is an indicatior of investor appetite for multifamily properties.

Though Multifamily Returns Have Declined, Long-term Fundamentals Remain Attractive

Source: National Council of Real Estate Investment Fiduciaries (NCREIF)

*Represents total returns as measured by the NCREIF Property Index (NPI), which reflects investment performance for over 10,000 commercial properties, totalling $933 billion of market value.

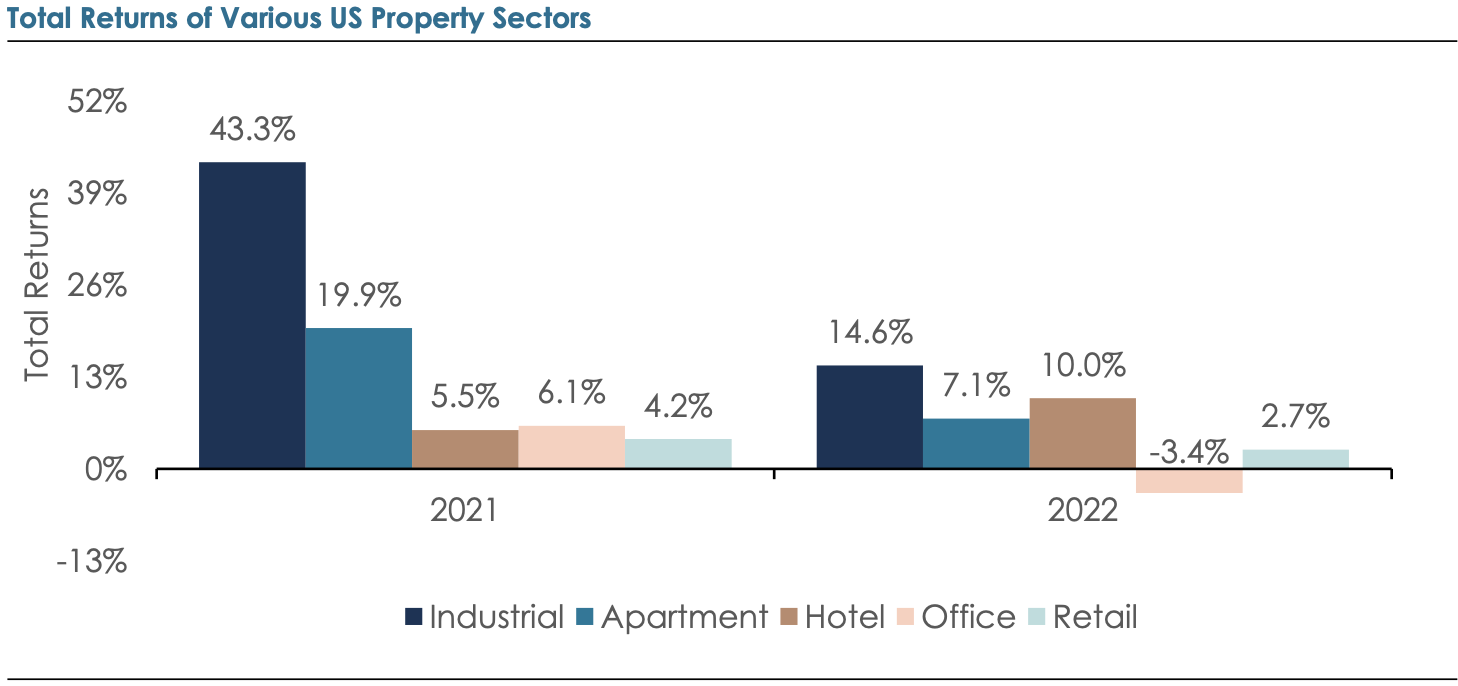

After delivering an exceptional performance in 2021, the total returns for the US apartment sector slipped to 7.1% in 2022 from 19.9% in 2021. Notably, the returns were negative in the fourth quarter of 2022 at -3.2%, compared to 6.8% return the sector delivered in the fourth quarter of 2021. Historical analysis provided by CBRE suggests that multifamily is one of the most promising sectors – having delivered an average annual total return of 9.3% over the past decade.

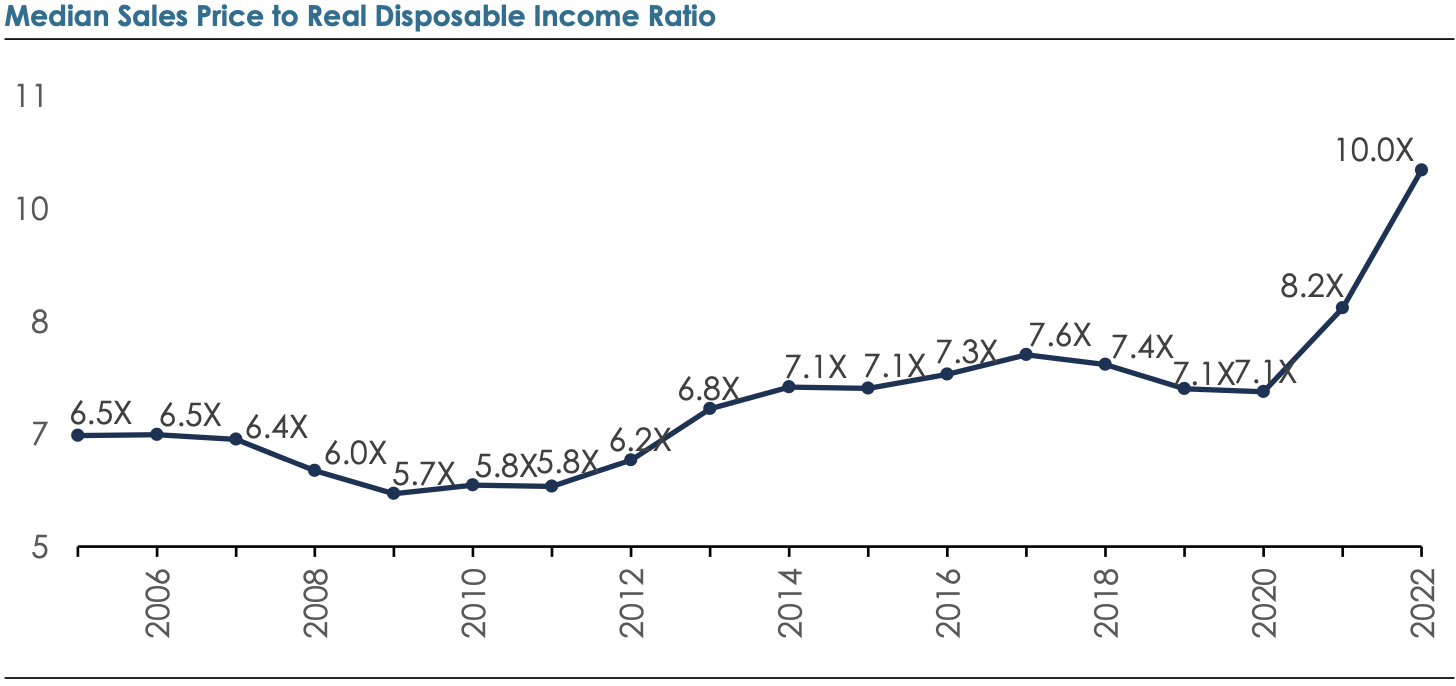

Housing Affordability Remains Out of Reach, Boding Well for Rental Demand

Source: FRED, Federal Reserve Bank of St. Louis

Note: Calculated by dividing median sales price of houses sold by real disposable personal income per capita

The ratio of median price of houses sold to disposable personal income per capita rose to all-time high in 2022, suggesting US housing affordability remains out of reach for majority of potential new homeowners. Since 2020, the ratio has increased by about 42% – from 7.1x to 10.0x in 2022.

Currently, the cost gap between the average payment for a newly purchased home and average monthly apartment rent is 37% (per April 2023 CBRE report). This is in contrast to the 8.5% premium that existed before the pandemic.

Outlook

Investors should remain cautious about the near-term prospects for multifamily properties and optimistic about its long-term prospects. The sector is expected to see a decline in demand during the first half of the year. However, as the market stabilizes, its relative durability might be evident in the middle to longer term.

Rising interest rates have restrained multifamily investment activity, as higher mortgage rates have kept home buyers and investors on the side-lines. According to research by Newmark, the new supply has surpassed demand over the past year resulting in a reduction in the absorption. The level of supply the market provides within the next 12-24 months will partly determine the duration of the challenges the multifamily market will face.

Nevertheless, the multifamily sector remains among one of the more resilient sectors within commercial real estate. The long-term tailwinds this sector remains intact, as there is a considerable shortage for mid-priced affordable housing in the US, which can eventually cater to the US’ large millenial and gen Z population. Interestingly, the multifamily sector was ranked as the top asset choice in the Americas in Colliers’ ‘2023 Global Investor Outlook’ report.